Axis Bank has released a first-of-its-kind study, Pink Capital: The Spectrum of Queer Money, showing how LGBTQIA+ communities in India earn, save, borrow, and spend. The report uncovers the lived financial realities of queer individuals and what true inclusion in banking looks like.

What is the Pink Economy?

The term Pink Economy refers to the economic activity generated by LGBTQIA+ individuals… not just as consumers, but as earners, investors, and participants in financial systems.

When Family Finances Leave You Out

In India, finance has long been tied to traditional family structures, which often leaves queer people excluded from wealth-building, inheritance, loans, and insurance. Personally, growing up, finance was never one of those conversations that you have at the table. It was only when I grew up and found myself facing financial roadblocks, did I realise that queer individuals face an additional layer of challenges. The challenges are as fundamental as opening a bank account or asking for a debit card with your chosen name!

Research Methodology

So with that experience, it was very interesting for me to go through the report. The report combines numbers with narratives through a layered methodology, from the Pegboard Picnic simulation with 50 community members, to dialogues with the TWEET Foundation, and conversations with experts.

The research methodology itself is refreshing. In one exercise called the Pegboard Picnic, gave community members ₹5,000 in symbolic “pink rupees” to spend on a given list of items in the market, however they wished to. It included items related to healthcare, housing and even celebrations.

Key Findings: What Does Queer India Want?

This small act revealed something huge: queer spending priorities aren’t just about buying rainbow-branded products or Pride merch. They’re about survival, dignity, and long-term stability. Healthcare, financial security, and safe housing were consistently top priorities.

And honestly, this is something that I have seen and felt for years. Not just me, but almost all of my queer friends too. Money is protection against being disowned. It’s a ticket to a chosen family when the biological one shuts their doors.

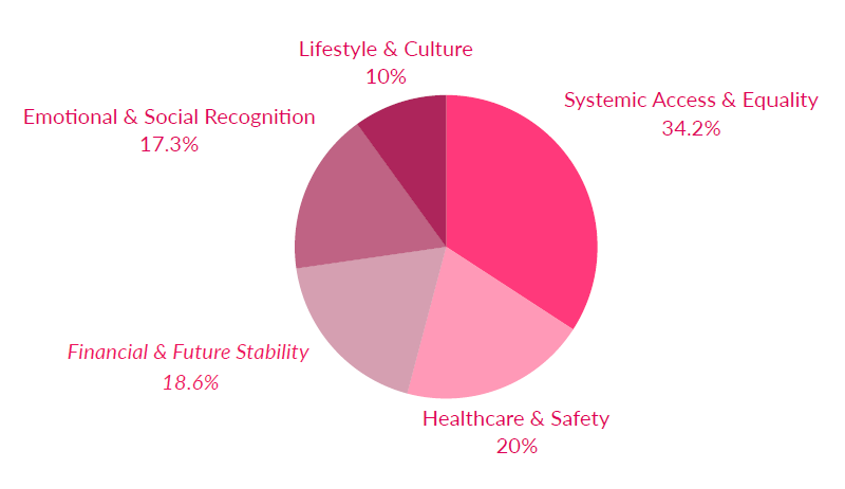

The report builds on Axis Bank’s ComeAsYouAre, a charter of policies and practices for employees and customers who are queer. Since this charter was announced in 2021, the bank has made facilities like joint accounts accessible for queer partners, including honorifics like Mx (which the bank noted, has been used by over 11,000 customers till date). And its findings reveal a hierarchy of queer financial needs, showing where inclusion is most urgent.

Systemic Access & Equality refers to having legal recognition of one’s identity, and having inclusive banking, housing, and education access.

Healthcare & Safety refers to receivinggender-affirming care, insurance coverage for partners, and inclusive wellness products.

Financial & Future Stability refers to access toqueer-focused loans, retirement products, and community housing models.

Emotional & Social Recognition refers to having validation in families, inclusive weddings, cultural milestones.

Lifestyle & Culture is about authentic representation in media, gyms, and consumer goods tailored to queer needs.

The message is clear: queer Indians want equal access to everyday financial tools that others take for granted.

As Harish Iyer, Senior VP and Head of Diversity, Equity & Inclusion at Axis Bank, puts it:

“Pink Capital is about identity, security, and the right to dream. By studying Pink Capital, we are moving the conversation from identity to impact.”

Is Queer Market Just Something To Be Tapped?

The report also talks about the lazy ole framing of queer money as just a “market to be tapped.” But NO, says the report. It is not about consumption, but circulation. Where does queer money flow? Where does it get blocked? And how can systems stop siphoning it back into heteronormative structures that implicitly exclude us such as family property laws, lack of inclusive retirement/insurance products.

The World Bank warns that discrimination against LGBTQIA+ people could cost India up to 1.7% of GDP annually.

This is a point that often gets overlooked in corporate Pride campaigns: visibility without access is just pinkwashing. India’s queer community holds an estimated $168 billion in purchasing power, yet systemic exclusion prevents this wealth from meaningfully benefiting the community itself. Too often, queer earnings are absorbed into heteronormative structures, siphoning away economic power instead of strengthening queer safety, dignity, and long-term stability. If money were allowed to circulate within the community, it could generate a powerful multiplier effect, fueling inclusion, resilience, and sustainable growth.

And the Cost of Exclusion?

The report highlights voices that make these insights real:

A couple opening a joint account, calling it “a quiet symbol of acceptance.”

A trans-woman stressing that transition care is life-saving, not cosmetic.

A gay entrepreneur dreaming of retirement homes where queer people can live openly.

These stories remind us that queer money is not abstract capital… It is tied to dignity, safety, and dreams for the future.

The report calls for banks, businesses, and policymakers to recognize queer Indians as full participants in the economy. It argues that inclusion feeds into the economy when queer individuals have equal access to products, services, and security, everyone benefits.

Other important points covered-

1. Intra-community diversity: The report also emphasizes how different it looks across the spectrum:

Class and caste divides: metro-based double-income-no-kids households vs. working-class queer/trans folks in informal jobs.

Trans experience: systemic barriers in ID documentation, healthcare, and employment far sharper than for cis gay/lesbian folks.

This diversity matters because the needs of a queer entrepreneur in Delhi and a trans sex worker in Panipat are worlds apart.

2. Borrowing & Credit Behavior

The report shows queer people save more, borrow less, often not out of choice but because loans/credit remain structurally harder to access (lack of documentation, lack of recognized partners/nominees, fear of outing).

3. It also points out concrete pathways to improve the policy and banking sector’s product opportunities such as:

Queer-affirming health products & insurance.

Housing models inclusive of queer folks.

Education/scholarships.

Workplace reforms.